Preferred Return – Simple Interest vs. Compound Interest

A concept common to real estate partnership structures, preferred return refers to the preference given to a certain class of equity partners when distributing available cash flow. The preferred return is generally calculated as either a percentage return on contributed capital or a given multiple on contributed capital, and must first be paid before common equity (i.e. the sponsor / general partner) has a right to promoted interest.

Simple Interest vs. Cumulative Interest When Calculating Preferred Return

How Preferred Return Fits in the Real Estate Waterfall

In a typical real estate partnership distribution waterfall, the preferred return comes first. For example:

- First, cash flow will be distributed to the partners in accordance with their partnership percentages until the Limited Partner has achieved an annualized, cumulative preferred return equal to 8.0% ; after which

- Second, excess cash flow will be distributed to the partners in accordance with their partnership percentages until each Partner’s capital account balance has been reduced to zero; after which

- Third, excess cash flow will be distributed (a) 75% to the partners in accordance with their partnership percentages, and (b) 25% to the General Partner as a promote until the Limited Partner has achieved a 12% internal rate of return; and

- Lastly, the balance will be distributed (a) 60% to the partners in accordance with their partnership percentages, and (b) 40% to the General Partner as a promote thereafter.

In the above example, all cash flow is distributed to the partners until the Limited Partner has earned an annual, cumulative preferred return of 8.0%. It is not until that preferred return has been hit, that the excess cash flow is available to pay down capital or pay promoted interest to the General Partner.

Check out a few examples of real estate waterfalls in our Library of Real Estate Financial Models

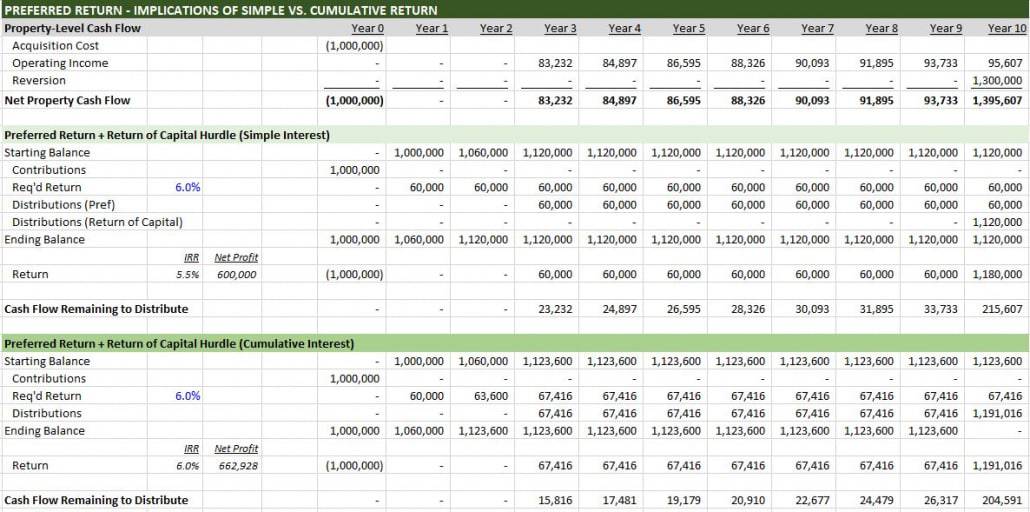

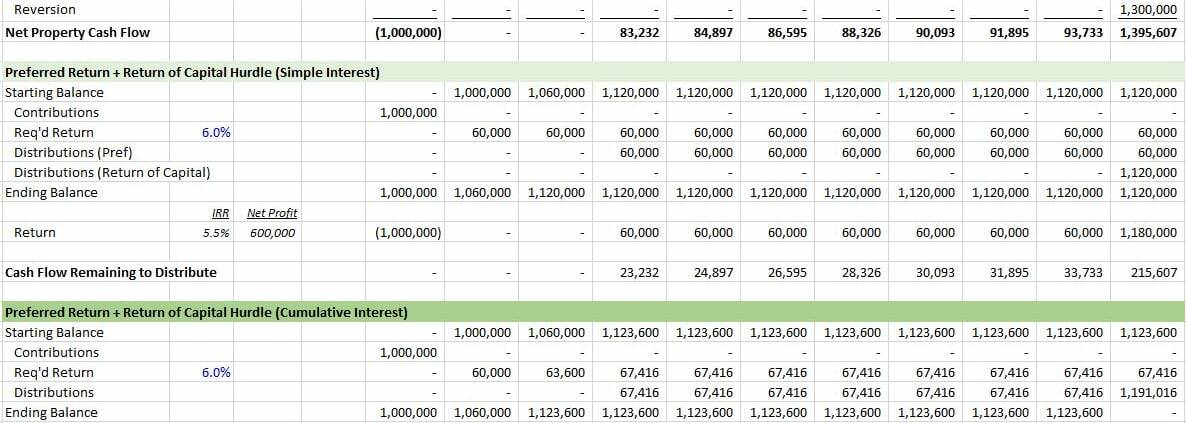

Implications of Simple vs. Cumulative Interest

There are various methods and metrics used to calculated preferred return. Preferred return is most often calculated as a percentage of contributed capital, but that return may be figured using simple interest (i.e. calculated on contributed capital to date) or using cumulative interest (i.e. calculated on contributed capital plus on any unpaid preferred return to date).

The resulting internal rate of return to the capital partner can be quite different between the two calculation methods, with the difference more pronounced in scenarios with insufficient cash flow in earlier years to cover the preferred return.

- Click here to download the example file used in this video